Update: 14 Jul 2024

Many people would agree that the first and foremost metric (some said the "only" metric) to look for in a REIT result statement, is that the DPU must be improved YoY and better yet QoQ. On the surface, it is true, if only all REITs standardize their way of distribution at all times. However, in reality, different REITs would have different policies on % of fees elected in units, % of retention, as well as a decision of distribution from divestment or income support, and all these changes from time to time. Today, let's go through these components of the distribution.

First, we would need to understand how REIT derives its distribution from the financial statement. To simplify, let's omit all those non-cash items like net changes in fair value for properties/financial derivatives, unrealized foreign exchange, depreciation, amortization as well as straight-line rental and etc. Note that all pictures below are not to scale.

Income Statement (Statement of Total Return/Profit & Loss)

1) Income of a REIT generally comes from gross revenue, interest income, income support and divestment gain. For income support, some REITs included this portion in their gross revenue, while some only do adjustments in the distribution statements.

2) Net property income (NPI), derived from deducting the property operating expenses from gross revenue.

3) After property operating expenses, the majority of remaining expenses come from manager management fees, trustee fees, finance expenses and tax. Deducting these expenses from NPI and adding the interest income, we would get the profit. I have termed it as "operating profit" as I excluded the divestment gain/loss and income support from the figure.

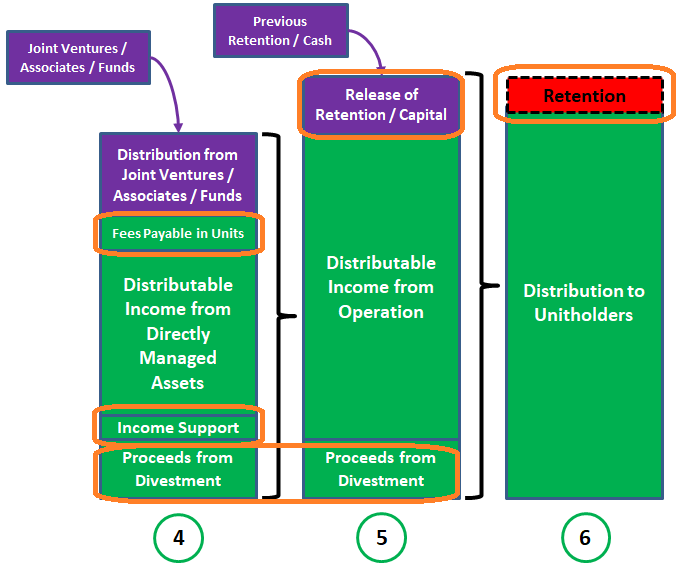

The gross revenue and NPI from the income statement only capture directly managed assets, excluding those assets which are managed by joint ventures, associates and funds. While there is "share of results of joint ventures/associates/funds" from the income statement, this amount is a non-cash item that includes valuation gain/loss and any unrealized gain/loss. Therefore it would be more appropriate to take the amount of distributions from joint ventures, associates and funds which could be obtained from the distribution statement or cash flow statement.

Distribution Statement

4) Continuing from the income statement, the distributions from joint ventures, associates and funds will be added, these amounts capture the distribution from those non-directly managed assets. Fees that are payable/paid in units would be added as well as these are non-cash items. These fees could include property management fees, manager management fees, etc. Whereas for proceeds from divestment, the manager can choose to distribute the proceeds as a capital return to unitholders whether the divestment is a gain or a loss.

5) Upon combining distributable income from directly managed assets and non-directly managed assets, income support and fees payable in units, the distributable income from the operation is derived. Management could also release previously retained distribution or some amount from the capital/cash. Do not consider all "capital distribution" as a capital/cash return to unitholders because certain income from foreign assets is being treated as a return of capital for Singapore income tax purposes.

6) As we all know, REITs are required to distribute at least 90% of taxable income for each financial year to enjoy tax benefits. In other words, management could retain some distribution for working capital, for up to 10% of taxable income. The distribution per unit (DPU) that unitholders would receive in the end, is the amount that divides the distribution to unitholders by the number of issuable/issued units.

Simplified Flow of Distribution Derivation

Let's combine both pictures and see the relation:

Now, I hope the above provides a clearer picture of how distribution is derived. It is simplified by omitting non-cash items which cover but not limited to fair value change of assets/derivatives, shares of results of joint ventures/associates/funds, depreciation and amortization as well as unrealized foreign exchange gain/loss, - Straight-line rental adjustments, etc.

Manipulatable Components

Next, we could start to identify which portions can the manager adjust/manage (or rather, manipulate in a blunt way of speaking) to increase/decrease the DPU. Let's look back at items 4,5,6:

Those components that could be managed is circled in orange as above:

1) Retention

This is the amount that managers retain mainly for working capital or conservation purposes, which could range up to 10% of taxable income as mentioned above.

2) Proceeds from Divestment

Managers can choose to distribute sales proceeds from the asset divestment to unitholders, partial or full, whether at a gain or a loss. The total amount is difficult to track as there might be multiple divestments among different periods and these proceeds are distributed across multiple periods.

3) Income Support

This is also named rental support or rental top-up, which could come in the form of a fixed amount or topping up the differences between actual vs expected rental (up to a specific limit) that spread across periods of time. The amount limit and the end period are to be taken note of as distribution would be affected once the amount is reached or the period has ended, whichever is earlier.

There is another way to increase DPU in which certain special unitholders would not be entitled to distribution during certain periods of time. I would consider this as a form of income support as well. This method was used by BHG Retail REIT and Dasin Retail Trust previously, and the income support ended in 2020 and 2021 respectively. You could refer to my previous post -

Case Studies for SREITs with Income Support if you are interested to know more.

4) Fees Payable in Units

The most common fees being paid in units would be the manager's base and performance fees. Some REITs also pay part of their property management fees to the property manager with units. In some cases, REITs would pay the management fees of joint ventures/associates in units as well.

5) Release of Retention / Capital

Sometimes, REIT would retain distribution in early quarters and release it at the later (or last) fiscal quarter. In some rare cases, REIT could choose to distribute from cash as well.

Surprisingly, there is quite a number of components that could be adjusted, isn't it? Enough of the theory, how about some case studies next?

Case Study

I have selected Frasers Centrepoint Trust and Frasers Logistics & Commercial Trust for practical examples.

1) Frasers Centrepoint Trust

From the income statement, gross revenue deducting property expenses is equal to net property income. Subsequently, adding interest income, deducting finance expenses and deducting fees would be the net income (profit before tax, fair value change and shares of results of joint ventures/associates).

For the distribution statement, REITs could use either of the below 3 to do distribution adjustment:

i) Net income before fair value change, shares of joint ventures/associates and tax

ii) Profit (or total return) before tax

iii) Profit (or total return) after tax

FCT uses net income before fair value change, shares of joint ventures/associates and tax, therefore, the NOTE A adjustment will not have to repeat those non-cash items to offset back. From the extract above, there are distributions from joint ventures/associates and manager's fees payable in units but no income support and partial proceeds from divestment. From the footnote, both the release of retention and retention are presented for the 2H 2022 period, where $4.8 mil is the release of retention while $ 1.7 mil is the retention.

2) Frasers Logistics & Commercial Trust

Basically, the income statement is similar to FCT, however, FLCT has no share of results of joint ventures/associates.

Unlike FCT, FLCT uses profit after tax in the distribution statement. Therefore, the NOTE A adjustment has these repeating non-cash items to offset back. FLCT has rental support and proceeds from divestment in the distribution. However, only "distributable income" is shown but no info on the "distribution to unitholders". Does FLCT retain any distribution in 2H 2022? One way to find out would be by dividing the amount by units in issue.

S$ 139,645,000 / 3,696,167 = S$ 0.0377 = 3.77 cents. From here we could see that the manager distributed 100% of the distributable income. Note that, for some REITs, issuable units are entitled to DPU too.

The other way to check the retention would be to read the distributions to unitholders records in the next financial statement, for e.g., from the distribution statement above, FLCT distributed S$ 142,108,000 for the period from 1 Oct 2021 to 31 Mar 2022.

Takeaway

A financial statement is always a dry topic, especially for people without prior experience, knowledge or interest in it. Therefore, I always prefer to simplify and use visuals to explain to readers. In my opinion, the financial statement of REITs, particularly those without joint ventures or associates is easier to understand than normal stocks.

So now that we understand the manipulatable components, can we say for sure that a DPU improvement is equal to good management or improving fundamental? Could it be due to partial proceeds from divestment or income support? Or more % of fees payable in units? Maybe the increase is due to lesser or no retention? It won't be a surprise that a REIT reports a 5-10% increase in DPU which is actually due to a lower retention amount and a higher % of fees elected in units. The same is applied to a DPU decline as well. Hate to say that, sometimes, details do matter.

Also, notice how different the distribution statement is even though both REITs above are under the same sponsor? Definitely, other REITs would have differences in their financial statement presentation as well. However, the structure would still hold the same, just in slightly different terms and arrangement.

Finally, if you have read this dry and long financial statement-related post till the end, thanks for your time. I hope this sharing is useful to you, feel free to

contact me if you have any queries.

You could also refer below for more information:

SREITs Dashboard - Detailed information on individual Singapore REIT

SREITs Data - Overview and detail of Singapore REIT

REIT Review - List of previous REIT review posts

And you could join the following to support my work:

Singapore REITs Post Telegram Channel - Join to receive posts for Singapore REITs

REIT-TIREMENT Patreon - Support my work and get exclusive content

REIT-TIREMENT Facebook Page - Support by liking my Facebook Page

REIT Investing Community - Facebook Group where members share and discuss REIT topic

*Disclaimer: Materials in this blog are based on my research and opinion which I don't guarantee accuracy, completeness, and reliability. It should not be taken as financial advice or a statement of fact. I shall not be held liable for errors, omissions and loss or damage due to the use of the material in this blog. Under no circumstances does the information presented on this blog represent a buy, sell, or hold recommendation on any security, please always do your own due diligence before any decision is made.

No comments:

Post a Comment