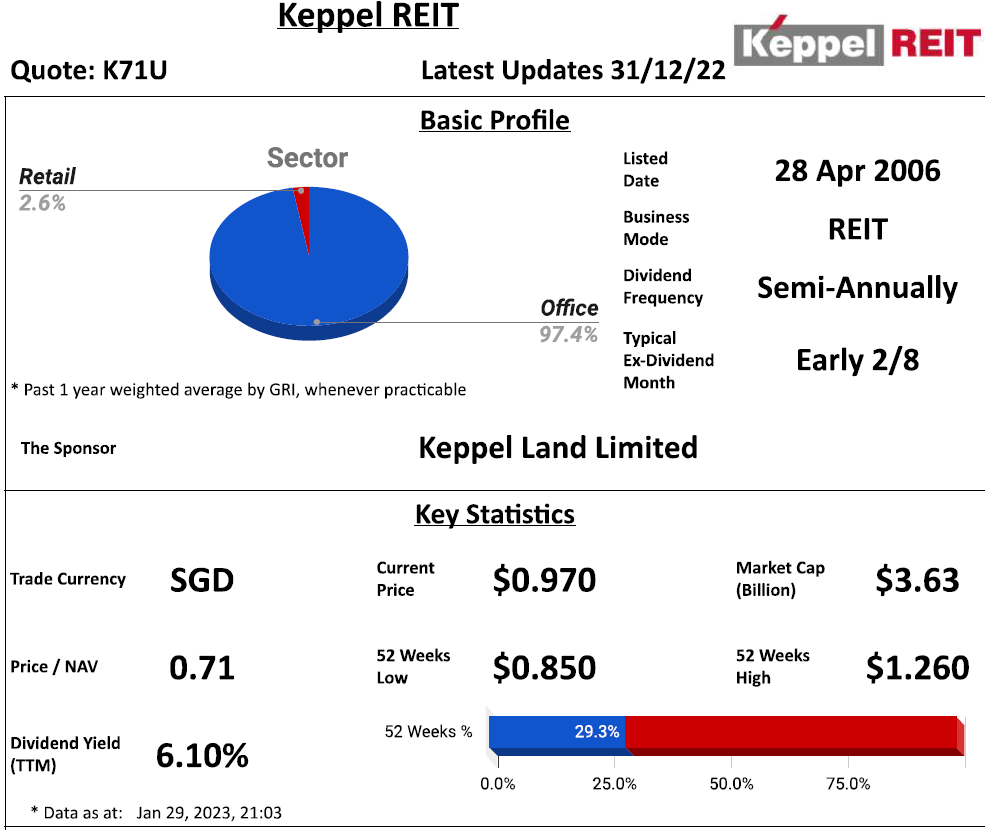

- Main Sector(s): Office

- Country(s) with Assets: Singapore, Australia, South Korea & Japan

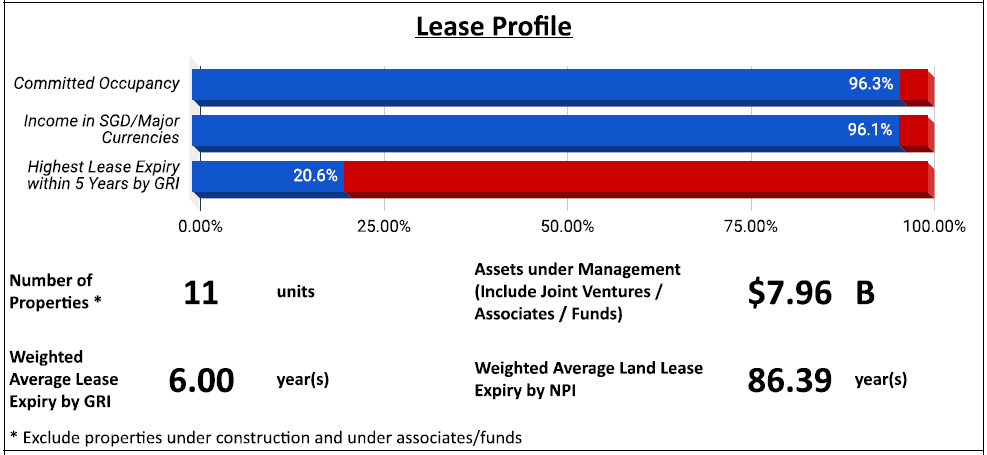

- No. of Properties (exclude development/associate/fund): 11

Key Indicators

- Distributable Income Breakdown:

- 70.9% from Operation

- 23.8 from Fees Paid/Payable in Units

- 0.8% from Income Support

- 4.5% from Proceeds from Divestment

- Distribution = 100% of Distributable Income

- Distribution to Perpetual Securities Holder = 4.3% of Distributable Income

Related Parties Shareholding

- REIT sponsor's shareholding: Above median for more than 20%

- REIT manager's shareholding: Above median for more than 20%

- Directors of REIT manager's shareholding: Below median for more than 20%

Lease Profile

- Occupancy: ± 5% from median

- WALE: Above median for more than 20%

- Highest lease expiry within 5 years: Below median for more than 10%; Falls in 2025

- Weighted Average Land Lease Expiry: Above median for more than 20%

Debt Profile

- Gearing ratio: ± 10% from median

- Gearing ratio includes perps: ± 10% from median

- Cost of debt: Below median for more than 20%

- Fixed rate debt %: ± 10% from median

- Unsecured debt %: ± 10% from median

- WADM: ± 10% from median

- Highest debt maturity within 5 years: Below median for more than 20%; Falls in 2024

- Interest coverage ratio: Below median for more than 10%

Diversification Profile

- Top geographical contribution: Above median for more than 20%

- Top property contribution: Above median for more than 20%

- Top 5 properties' contribution: Above median for more than 20%

- Top tenant contribution: Below median for more than 20%

- Top 10 tenants' contribution: ± 10% from median

Key Financial Metrics

- Property yield: Below median for more than 20%

- Management fees over distribution: Above median for more than 20%; $4.20 distribution for every dollar paid

- Distribution on capital: Below median for more than 20%

- Distribution margin: Above median for more than 20%

Trends

- Uptrend: Interest Coverage Ratio, Property Yield

- Slight Uptrend: DPU, Distribution on Capital

- Slight Downtrend: NAV per Unit, Occupancy

- Downtrend: Distribution Margin

Relative Valuation

- P/NAV: Below average for 1y; Below -1SD for 3y & 5y

- Dividend Yield: Above average for 1y; +1SD for 3y; Above for 2SD for 5y

Author's Opinion

| Favorable | Less Favorable |

|---|---|

| High REIT Sponsor's Shareholding | Low Directors of REIT Manager's Shareholding |

| High REIT Manager's Shareholding | Low Interest Coverage Ratio |

| Long WALE | High Top Geographical Contribution |

| Well Spread Lease Expiry | High Top Property & Top 5 Properties Contributions |

| Long Weighted Average Land Lease Expiry | Low Property Yield |

| Low Cost of Debt | Non Competitive Management Fees |

| Well Spread Debt Maturity | Low Distribution on Capital |

| Low Top Tenant Contribution | Distribution Margin Downtrend |

| High Distribution Margin | |

| Interest Coverage Ratio Uptrend | |

| Property Yield Uptrend |

Property income and NPI improved slightly as compared to the previous quarter. As per the previous announcement, the manager will distribute the "anniversary distribution" starting from this distribution, which helps to cushion the borrowing cost increase and increasing cost.

For more information, check out:

SREITs Dashboard - Detailed information on individual Singapore REIT

SREITs Data - Overview and details of Singapore REIT

REIT Review - List of previous REIT review posts

Singapore REITs Post Telegram Channel - Join to receive posts for Singapore REITs

REIT-TIREMENT Patreon - Support my work and get exclusive content

REIT-TIREMENT Facebook Page - Support by liking my Facebook Page

REIT Investing Community - Facebook Group where members share and discuss REIT topic

*Disclaimer: The information presented on this blog is for educational and informational purposes only. The materials, including research and opinions, are based solely on my own findings and should not be considered as professional financial advice or a definitive statement of fact. I cannot guarantee the accuracy, completeness, or reliability of the information provided. I shall not be held liable for any errors, omissions, or losses that may occur as a result of using the information presented on this blog. It should be noted that the information presented on this blog does not constitute a buy, sell, or hold recommendation for any security. It is crucial to conduct your own thorough research and due diligence before making any investment decisions.

No comments:

Post a Comment