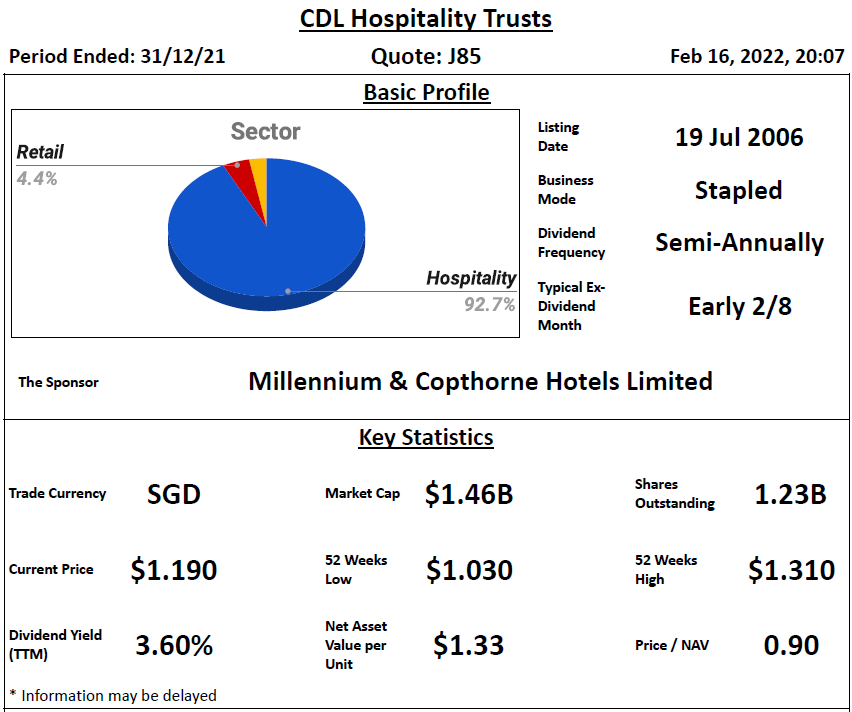

Basic Profile & Key Statistics

Performance Highlight

- REIT sponsor's shareholding is high at 38.21%

- REIT manager's shareholding is high at 8.027%

- Directors of REIT manager's shareholding is low at 0.011%

Lease Profile

- WALE is long at 4.76 years

- Highest lease expiry within 5 years is moderate at 26% which falls in 2022

- Weighted average land lease expiry is slightly long at 79.85 years

Debt Profile

- Gearing ratio is moderate at 39.1%

- Cost of debt is low at 2%

- Fixed rate debt % is low at 61.3%

- Unsecured debt % is slightly high at 83.6%

- WADM is short at 2.1 years

- Highest debt maturity within 5 years is high at 38.3% which falls in 2022

- Interest coverage ratio is low at 3.3 times

Diversification Profile

- Top geographical contribution is low at 43.4%

- Top property contribution is low at 14%

- Top 5 properties contribution is low at 50.6%

- Top tenant contribution is high at 20.7%

- Top 10 tenants contribution is high at 93.4%

- Top 3 countries contribution is from Singapore, England and New Zealand which contribute more than 70% of GRI

Key Financial Metrics

- Property yield is low at 3.2%

- Management fees over distribution is high at 18.9% in which unitholders receive S$ 5.29 for every dollar paid

- Distribution on capital is low at 1.9%

- Distribution margin is low at 25.4%

- 23.8% of the past 12 months DPU is from distribution from asset disposal

Trends

- Downtrend - DPU, NAV per Unit, Interest Coverage Ratio, Property Yield, Distribution on Capital, Distribution Margin

Relative Valuation

- P/NAV - Average for 1y, 3y and 5y

- Dividend Yield - Below -1SD for 1y, 3y and 5y

Author's Opinion

| Favorable | Less Favorable |

|---|---|

| High REIT Sponsor's Shareholding | Low Directors of REIT Manager's Shareholding |

| High REIT Manager's Shareholding | Low Fixed Rate Debt % |

| Long WALE | Short WADM |

| Low Cost of Debt | Concentrated Debt Maturity |

| Low Top Geographical Contribution | Low Interest Coverage Ratio |

| Low Top Property & Top 5 Properties Contributions | High Top Tenant & Top 10 Tenants Contributions |

| Low Property Yield | |

| Non-Competitive Management Fees | |

| Low Distribution on Capital | |

| Low Distribution Margin | |

| High Distribution from Asset Disposal | |

| DPU Downtrend | |

| NAV per Unit Downtrend | |

| Interest Coverage Ratio Downtrend | |

| Property Yield Downtrend | |

| Distribution on Capital Downtrend | |

| Distribution Margin Downtrend |

Generally, the performance and REVPAU have improved in 4Q. However, due to Omicron, some countries have implemented temporary restrictions starting December 2021. Do note that CDLT has distributed S$ 12.5 mils of divestment gain in FY 21, which amounts to 23.8% of FY21 distribution.

You could also refer below for more information:

SREITs Dashboard - Detailed information on individual Singapore REIT

SREITs Data - Overview and Detail of Singapore REIT

REIT Analysis - List of previous REIT analysis posts

Singapore REITs Post Telegram Channel - Join to receive posts for Singapore REITs

REIT-TIREMENT Patreon - Support my work and get exclusive contents

REIT-TIREMENT Facebook Page - Support by liking my Facebook Page

REIT Investing Community - Facebook Group where members share and discuss REIT topic

*Disclaimer: Materials in this blog are based on my research and opinion which I don't guarantee accuracy, completeness, and reliability. It should not be taken as financial advice or a statement of fact. I shall not be held liable for errors, omissions and loss or damage as a result of the use of the material in this blog. Under no circumstances does the information presented on this blog represent a buy, sell, or hold recommendation on any security, please always do your own due diligence before any decision is made.

No comments:

Post a Comment