Basic Profile & Key Statistics

Lease Profile

Occupancy is moderate at 92.6%. WALE is slightly low at 3.6 years where the highest lease expiry of 38.8% falls in 2024 and beyond, without breakdown. Weighted average land lease expiry is moderate at 61.94 years.

Debt Profile

Gearing ratio is slightly high at 40.3%. Cost of debt is high at 3.1% with a low % of unsecured debt at 40.8%. Fixed rate debt % is moderate at 76.3%. Interest cover ratio is low at 2.7 times. WADE is short at 1.6 years where the highest debt maturity of 30% falls in 2021.

Diversification Profile

91.3% of its income is from Singapore properties and remaining is from Lippo Plaza in China. Top property, top tenant and top 10 tenants contribution are high at 24.3%, 25.7% and 50.8%.

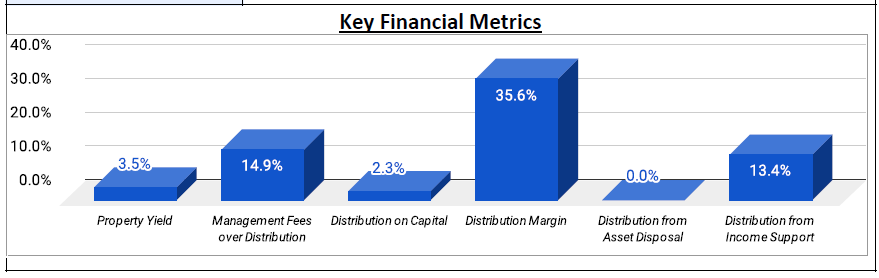

Key Financial Metrics

Property yield, distribution on capital and distribution margin are low at 3.5%, 2.3% and 35.6% respectively. Management fee is moderate in which unitholders receive S$ 6.71 for every dollar paid to the manager. 13.4% of the past 4 quarters DPU is from income support. Including retention of S$ 10.8 million, figures for management fees over distribution, distribution on capital, distribution margin and income support would be 13.4%, 2.4%, 40.1% and 12.1%.

Trends

Flat - NAV per Unit

Slight Downtrend - Interest Cover Ratio

Downtrend - DPU, Property Yield, Distribution Margin

Relative Valuation

i) Average Dividend Yield - Average yield at 7.15%, apply the annualized past 4 quarters DPU of 2.45 cents will get S$ 0.345. Including retention, the DPU would be 2.65 cents which translates into S$ 0.37.

ii) Average Price/NAV - Average value at 0.7, apply the latest NAV of S$ 0.609 will get S$ 0.425.

Author's Opinion

| Favorable | Less Favorable |

|---|---|

| Diversified Sector | High Cost of Debt |

| Low Unsecured Debt % | |

| Low Interest Cover Ratio | |

| Short WADE | |

| High Top Geographical Contribution | |

| High Property Contribution | |

| High Top Tenant & Top 10 Tenants Contribution | |

| Low Property Yield | |

| Low Distribution on Capital | |

| Low Distribution Margin | |

| More than 10% Income Support | |

| DPU Downtrend | |

| Property Yield Downtrend | |

| Distribution Margin Downtrend |

OUECT performance is affected mainly by its hospitality sector. Nonetheless, the performance has been improved on QoQ basis. With the recent positive news on vaccine coupled with more and more green land openings, the hospitality and retail sectors' performance should be improved. As for the office sector, the improvement in occupancy and positive rental reversion should also help in boosting its performance.

For more information, you could refer to:

SREITs Dashboard - Detailed information on individual Singapore REIT

SREITs Data - Overview of Singapore REIT

REIT Analysis - List of previous REIT analysis posts

REIT-TIREMENT Patreon - Support this blog as a Patron and get SREITs Dashboard PDF

REIT Investing Community - Facebook Group where members share and discuss REIT topic

*Disclaimer: Materials in this blog are based on my research and opinion which I don't guarantee accuracy, completeness, and reliability. It should not be taken as financial advice or a statement of fact. I shall not be held liable for errors, omissions as well as loss, or damage as a result of the use of the material in this blog. Under no circumstances does the information presented on this blog represent a buy, sell, or hold recommendation on any security, please always do your own due diligence before any decision is made.

No comments:

Post a Comment