Basic Profile & Key Statistics

Performance Review

Lease Profile

- Occupancy is slightly high at 95.1%

- WALE is long at 4.9 years

- Highest lease expiry within 5 years is high at 58.6% which falls in 2025 and beyond, without breakdown.

- Weighted average land lease expiry is long at 93.6 years

Debt Profile

- Gearing ratio is moderate at 38.1%

- Cost of debt is low at 1.7%

- Fixed rate debt % is high at 100%

- Unsecured debt % is high at 91%

- WADE is long at 3.8 years

- Highest debt maturity within 5 years is high at 36.2% which falls in 2022

- Interest coverage ratio is high at 6.4 times

Diversification Profile

- Top geographical contribution is low at 9.1% (from 2019 Annual Report)

- Top property contribution is low at 8.4% (from 2019 Annual Report)

- Top tenant contribution is high at 13.2%

- Top 10 tenants contribution is low at 33.8%

- Top 3 countries contributed around 68% of GRI

Key Financial Metrics

- Property yield is slightly high at 5.6%

- Management fees over distribution is competitive at 5.9% in which unitholders receive €16.95 for every dollar paid

- Distribution on capital is high at 4.1%

- Distribution margin is slightly low at 46.2%

- 3.2% of the past 4 quarters' distribution is from asset disposal.

Trends

- Slight Uptrend - Interest Coverage Ratio

- Downtrend - DPU, NAV per Unit, Property Yield, Distribution on Capital, Distribution Margin

Relative Valuation

- Dividend Yield - Past 4 quarters DPU @ 3.484 cents / average yield @ 8.14% = € 0.43

- Price/NAV - NAV @ €$ 0.509 x average P/NAV @ 0.95 = € 0.485

Author's Opinion

| Favorable | Less Favorable |

|---|---|

| Diversified Sector | Concentrated Debt Maturity |

| Long WALE | High Top Tenant Contribution |

| Long Weighted Average Land Lease Expiry | DPU Downtrend |

| Low Cost of Debt | NAV per Unit Downtrend |

| High Unsecured Debt | Property Yield Downtrend |

| Long WADE | Distribution on Capital Downtrend |

| High Interest Coverage Ratio | Distribution Margin Downtrend |

| Low Top Geographical Contribution | |

| Low Top Property Contribution | |

| Low Top 10 Tenants Contribution | |

| Competitive Management Fee | |

| High Distribution on Capital |

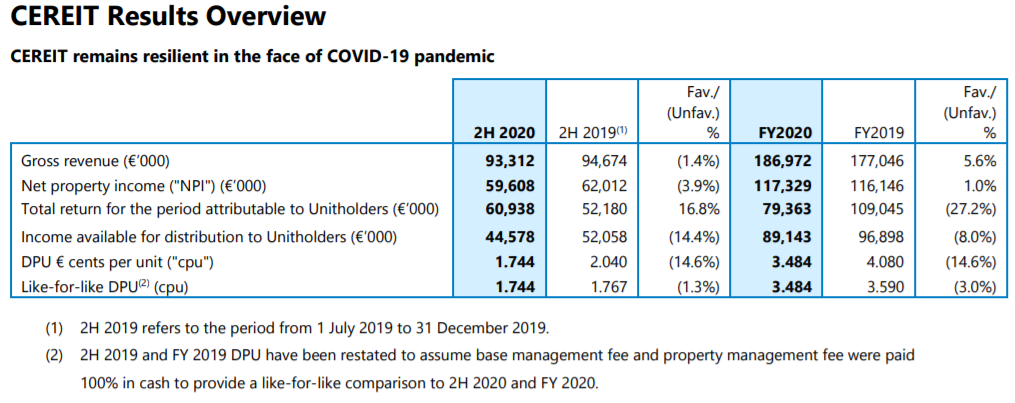

The main reason for DPU decrease is due to both base management fees and property management fees had been paid 100% in cash for FY 2020. Overall, CEREIT fundamentals remain healthy at this moment. As for the private placement, it is at 0.21% DPU accretive (pro forma) based on the issued price of € 0.44. And since the final issued price is fixed lower at € 0.43, the DPU accretion (or dilution) would be insignificant.

For more information, you could refer to:

SREITs Dashboard - Detailed information on individual Singapore REIT

SREITs Data - Overview of Singapore REIT

REIT Analysis - List of previous REIT analysis posts

REIT-TIREMENT Patreon - Support this blog as a Patron and get SREITs Dashboard PDF

REIT Investing Community - Facebook Group where members share and discuss REIT topic

*Disclaimer: Materials in this blog are based on my research and opinion which I don't guarantee accuracy, completeness, and reliability. It should not be taken as financial advice or a statement of fact. I shall not be held liable for errors, omissions as well as loss or damage as a result of the use of the material in this blog. Under no circumstances does the information presented on this blog represent a buy, sell, or hold recommendation on any security, please always do your own due diligence before any decision is made.

No comments:

Post a Comment